This page (maintained by my healthshare expert Bill) will dig further into the details of Sedera health sharing , and serve as a place to ask and answer questions in the comments section below.

After learning everything you need to know about the company, you can sign up with Sedera at the best possible prices, here:

https:/sedera.community/thefireguild1

(Sedera also has an option with a different enrollment process for employers. If you run a business and you’re interested, send an email to info@thefireguild.com for more info.)

*note: Sedera does pay its affiliates a small referral fee for new customers, which does not affect your monthly bill – in fact, this link offers a lower price than subscribing directly through the company’s website. Thus, we believe this is the lowest cost way on the Internet to get this coverage. In addition, we donate 10% of our gross revenue to RIP Medical Debt.

If you prefer a colorful, easy-to-read, cartoon-y overview, click here and you’ll learn ALL YOU NEED TO KNOW.

Otherwise, read on!

Sedera Update From a Real User – September 2022

Sedera seems unbelievable – a system for sharing medical costs at a fair price, run by people who are on my side? Too good to be true, right?

Here’s a quick story of my personal, recent (2022) experience with Sedera.

Quick facts: I’m 54, I’ve been a Sedera member for several years and as a member I pay for the first $1500 of any medical event. Sedera shares the cost of the balance. It’s really that easy. If you want more background, read on.

—

I had started feeling strange heartbeats and went to see my PCP (Primary Care Physician – who is a DPC – Direct Primary Care doctor). We made the decision together for me to get some cardiac tests done: A “stress-echo” (an in-person ultrasound of my heart beating while they pushed me to run increasingly faster on a treadmill, while hooked up to a bunch of wires like some bionic man) and a 2-week EKG using a very cool new technology called a Zio patch – a small device that was taped to my chest to record every beat and search for irregularities.

I shopped around, calling three different providers in my area of Southern Maine to find the best price and scheduling for the stress echo. Of course on the day of my test, they could not provide me a detailed bill for services and I immediately began to worry that the price they had quoted on the phone (after being transferred several times to try to get an answer to the “how much will this cost?” question) would not be honored. It turns out I was right.

A few days after the test, I received a massively inflated invoice from the provider (not a great feeling to a guy with heart trouble!) and got in touch with Sedera’s patient advocacy team to start negotiating on my behalf. They contacted the provider, handled all the calls/documentation and ended up with a significant discount. A new bill was sent to me, I paid with my credit card and provided the receipt to Sedera through their online portal.

For the Zio patch, it seemed I could only get it from a local cardiologist – again at a HUGE markup. Instead I simply searched for the product, went to the company’s site and found that they have a direct-to-patient service (with a cash discount) for a flat fee of $495. I ordered the patch which arrived two days later in the mail, and followed the easy instructions to affix it to my chest. After two weeks, I peeled it off and mailed it back in the prepaid mailer. They provided the results to my PCP (again, a DPC in my case) and we reviewed them. I submitted the receipt to Sedera and settled in for what I thought would be a long wait and a lot of back-and-forth.

I was mistaken.

Less than two weeks later, I woke up to see that the balance between what I paid, minus my $1500 IUA (Initial Unshareable Amount) had been directly deposited into my bank account! Done. It really was that easy and they really did simply send me the $ and SO much faster than any other experience I have had with reimbursement or insurance claims (have you ever dealt with car insurance? Ugh).

This was not a complete surprise, since my wife had a similar experience with Sedera sharing some medical costs in 2021, but in the meantime I had heard stories of bankruptcies caused by the unethical (in my opinion), exorbitant billing by the US healthcare system. We are trained to just accept that medical costs in the US are astronomical but inevitable – that the fear of losing everything due to an accident or illness is the Way Things Are. And, that our only hedge against this is to pay for mostly (hopefully) unused health insurance which for my family would be an assured $30K MINIMUM per year, regardless of our level of health.

Sedera shows that this doesn’t have to be the only way, and I believe it’s one of several systems that will eventually disrupt our current dysfunctional disconnect between providers and patients.

I know I said at the beginning that this would be a quick story and you may not think so after reading all of this. However, if you talk to anyone who has actually USED their insurance for anything beyond routine checkups, they’ll tell you much longer stories about excessive paperwork, billing discrepancies, arguing with their insurance company about what’s covered, “surprise” bills from out of network providers, etc.

In conclusion, I’m very happy with Sedera and the system has worked exactly as described. I am spending FAR less for the peace of mind that insurance plays in our lives and I know that should problems arrive in the future, Sedera will be there to help.

I signed up with Sedera several years ago and as I got to know the company better from my extensive research, a friend and I decided to start our own company – The Fire Guild. If you want to join Sedera, be sure to visit our site: www.thefireguild.com to learn all there is to know. There you’ll find out how it works, what it costs and if you want, how to directly contact Jon or me to ask whatever questions you may have.

(end of September 2022 update)

Bill here! As a long-time FIRE advocate, here’s what I like about Sedera:

- Cheaper than traditional health insurance (75% cheaper in some cases)

- No religious commitment or affiliation

- No network: Use any provider you like, anywhere (including internationally)

- Timely payment of eligible expenses

- A+ Rating from the Better Business Bureau

- Easy sign up

- Clear, easy-to-understand sharing guidelines

- No open enrollment or difficult-to-understand packages

- Preventive care (mammograms, colonoscopies, and flu shots)

- Expert second opinions

- Web-based interface for tracking bills, needs, and payments

- Responsive, US-based customer support (in Austin, TX)

- Transparency and low profit margins – your dollars go to helping members in need

- Membership growth has been organic to ensure that members are a good fit

- Discounted rates from providers (over two decades of experience negotiating medical bills)

- Supports healthy lifestyles by rewarding good behavior (non-smokers pay less, DPC members get a discount)

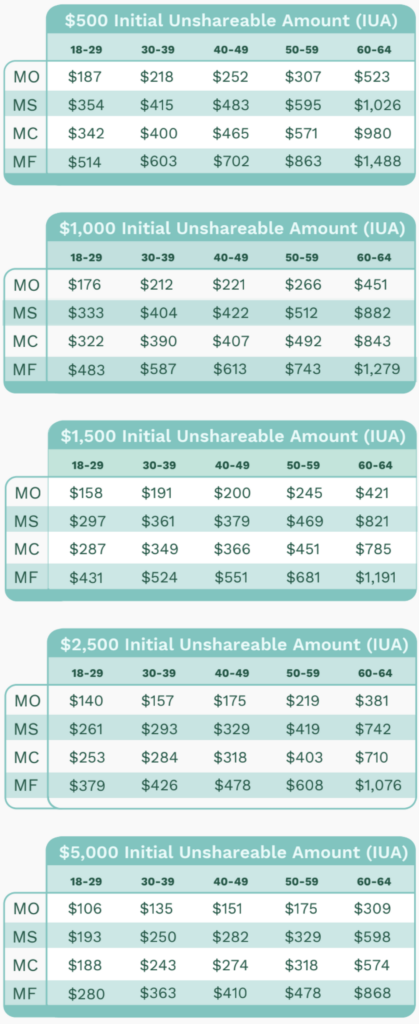

- Choices from $500 to $5K IUA allowing peace of mind for every budget

- Great option for the self-employed and FI seekers. Protect your assets!

- Only one raise in rates in 4 years

- Telemedicine (through publicly traded Teladoc, the first and largest telemedicine company in the US)

- Rx help

- Up to $750 in mental health assistance

- International care is covered

Why I Joined Sedera, or how I got better service for less money

My family joined Sedera because we needed some sort of coverage but the ACA was just too expensive. I’m in my early 50s, retired, and we were paying over $2K/month with a high deductible. At first I was attracted to Liberty (the least religious of all the Christian Health Sharing Ministries) but had moral difficulties with their exclusion of non-religious people (and their stance on certain women’s health issues). Why should religion have anything to do with health?

So, I searched and found Sedera. Secular, more agile, with an A+ BBB rating and on top of it all, cheaper! We now have excellent care through two local DPCs and complete assurance about catastrophes through Sedera.

Why Sedera is great for Mustachians or brass tacks; what does it really cost?

Self employed? Just quit your job and can’t deal with the hassle and expense of COBRA? Early retiree? Sedera works for you because you can sign up any time – there is no open enrollment period. Also, guess what? The prices are low. Like so low you’ll start to wonder why standard insurance is so expensive (and that kind of wonder is probably why you’re here in the first place). A quick example: 34 year old, single, member of a DPC, with a $2500 IUA: $157 per month! Below are prices for members of a DPC (MO is Member Only, MS is Member +Spouse, MC is Member+Children MF is Member+Family):

How Care and Payments Work (compared to insurance)

You’re probably already familiar with how health insurance works, and Sedera has some similarities though it’s not insurance. Think of Sedera as a group of your healthy friends who want to pool their resources to share health-related needs. In fact, with Sedera, when you have a medical bill you submit it (online – you have your own private portal) as a “Need”. Once approved, Sedera sends you your “Share”. Depending on your level of membership, you have an IUA (Initial Unshareable Amount) and just as you guessed, this is the dollar amount that you’re responsible for before you can submit a Need to be Shared. There are many more details about the number of Needs you are responsible for in a calendar year, what’s an acceptable Need, how quickly your Share arrives and more – the best way to learn about that is to read some of the FAQ’s below, or head over to https:/sedera.community/thefireguild1 and follow the links there. If you need more info or something’s not clear, ask here! (and if enough people ask, it will get rolled into the DFD* below)

*Devil-Free Details, or Frequently Asked Questions [NOTE: We will be updating the FAQ as questions come in (and seem suitable for this format). If the FAQ answers a particular set of comments, those will be removed in order to make this page more readable. Of course, almost every question can be answered in the Sedera Membership Guidelines, but we’d like to introduce you to the most frequent questions without having to go for the deep dive right off the bat!]

Q: How do I know Sedera won’t take my money and run?

A: This is one of the most common questions so we’ve put it here first. The answer is: You don’t. Sedera is not insurance and is not regulated. They have super scary, upfront ALL CAPS disclaimers on their site to make sure you understand the risks (and they want all members to actively CHOOSE to join). In order to keep their prices low (which was initially my main reason for joining), they have limitations and some of those would run up against the rules surrounding insurance. As such, they *have* to clearly post that they are NOT INSURANCE, etc.

If that scares you off as soon as you read it, then you can skip the rest and move on. However, if you’re a discerning consumer (of course you are, you’re on this blog!), you will read on and see that there’s a lot to calm your concerns: They’ve been in business for over six years (and their executive team has decades of health care experience), with no lawsuits, no complaints and they were even nominated for the coveted BBB Torch award for ethics. They have 35K members (and growing) and if they were in the business of taking your money and not providing services, our tried-and-true free market system would crush them like a bug. They’re totally transparent with their pricing and their guidelines. Plus, all operations are 100% US-based in Austin, TX and you can call them and they’ll answer. Think about how all of those points compare to your current health insurance provider!

Q: How long does it take to sign up, and what will I need?

A: If you’re a smart person (of course you are) who knows how to navigate the web and has filled out an online form before (ditto), then I’d suggest setting aside 15 minutes to go through the educational materials and then sign up at this link. You’ll need your SSN, bank account info, a credit card and some basic knowledge about your family. It’s really easy (particularly if you compare it to signing up for health insurance). However, it’s not currently available in Illinois, New York, Washington, Vermont. But they’re working on it!

Q: When does membership start?

A: Membership starts immediately, just like signing up with a DPC (or car insurance, Spotify, etc). Alternatively, you can sign up today and choose your future membership start date.

Q: Are there limitations on when I can sign up? Can I jump in the day after I quit my job, regardless of when that is? (Congratulations, btw!)

A: There’s no “open enrollment” or any other limitations – it’s very straightforward (as it should be). Skip COBRA and join up, or finally get some peace of mind as a gig worker or self-employed person. You can pay with a credit card or your bank account and you will be billed monthly on the date you signed up.

Q: How do I pay? Can I use a credit card?

A: Yes! You can pay with a credit card or your bank account and you will be billed monthly on the date you signed up. It’s all automated and very much like other memberships you’re familiar with (and unlike the reams of legalese and paperwork you’ve maybe dealt with in the past).

Q: What’s included without meeting my Initial Unshareable Amount?

A: Well-patient mammograms, colonoscopies, flu shots and other wellness events are included 100% – no need to reach your IUA first. You can read about what’s specifically allowed (and not) in Sedera’s Membership Guidelines. My 52-year-old wife recently had a routine mammogram. She made the appointment, stated she was an uninsured, cash-pay customer and secured a fantastic price which she paid for with her credit card. We submitted the two bills (imaging and the “reading” of the images) to Sedera via our private portal (snapped pics with the mobile phone) and received payment (check or direct deposit, your choice) 18 days later.

Q: What if I need a million dollar total head transplant? Are there any caps to how much will be shared?

A: In short, you pay your IUA and Sedera Members share the rest (aka you receive payment). There is NO UPPER LIMIT on a Need. Period. How can this be? Sedera has an entire group that helps negotiate pricing on major health events, and as such, that huge price is usually significantly reduced. Remember, hospitals and other health service providers are just running a business and given the chance to negotiate for faster payment often means they’ll offer a better rate.

Q: So I have a $1500 IUA; does that mean I have to pay that much of each bill I submit?

A: No way! Your $1500 IUA is per Need. So if you have a heart attack, that counts as a single need. You may continue to get treatment for that issue for a year (or more); all bills associated with that Need are included under your single IUA. You pay $1500 and the rest is shared.

Q: What about pre-existing conditions (PEC)?

A: You CAN sign up for Sedera if you have a PEC.

Sedera limits sharing for any PEC treated in the 3 years before signing up. You can totally sign up and have everything else shared, just not that condition during your first year of Membership. However, during the second year, you are eligible for $15k of Sharing, the third year $30k, and once you start your fourth year of membership, it would be fully shareable.

Q: What else is excluded?

A: A quick answer is: Anything illegal. If you are injured doing an illegal activity or from the use of illegal drugs, you’re on your own. I like this feature: It makes fellow members accountable for their own actions. There are detailed specifics in the guidelines, which are thorough but written in everyday language and are required reading before you sign up. Sedera doesn’t want just anyone – members are committed to taking responsibility for their own health and by extension, the other members of the community.

Q: What’s my maximum annual expense?

A: You’re responsible for your IUA for each Need, but only for a maximum of three Needs per year (including for Families). For example, if you have a $500 IUA you pay the first $500 for your broken leg on January 1st, the first $500 for your kidney stones in March and the first $500 for your broken arm in April. After that (what a bad year!), you are no longer responsible for any more IUAs on subsequent needs (if you continue to have bad luck). Your total out-of-pocket expense for your three bouts of bad karma payback will cost a total of $1500, regardless of how long your recovery is or how much it costs. Of course, you’re also responsible for your Monthly Contribution throughout your Membership period.

Q: What about maternity and pregnancy costs?

A: This is a big question and deserves a big answer but here’s the quick and general response: Sedera considers births, maternity and prenatal care shareable, but does not share in voluntary terminations. All pregnancies are subject to a $5K IUA ($7500 for non-emergency C-sections). This is to discourage people who join just to have their maternity costs shared, then leave the community.

Q: What’s their stance on prescriptions?

A: Sedera separates medications into two groups: curative and maintenance. Loosely explained, they share the former until you’re better. If a medication is initially prescribed to cure an ailment, it’s included, but if it becomes a maintenance drug, then only 120 days of that prescription will be shared. Some simple examples of curative drugs are antibiotics, pain meds and even chemotherapy. Statins, insulin and birth control (unless prescribed for a curative issue) would be considered maintenance drugs. Also, as an active member, you have access to Sedera’s RX Marketplace, where you’ll find incredible resources for inexpensive prescriptions, diabetic supplies and more.

— — —

I’ll continue to update this as I find comments that seem to stand out or get repeated. I am starting a site of my own, dedicated to Sedera, called The Fire Guild. My partner Jon may be helping me answer your comments and questions.

Final note from MMM: This is an ongoing experiment, with the goal of sharing something that is hopefully very beneficial to readers, so both positive and negative stories are welcome. Please share details that will be relevant to others – we’re all looking for information!

Jill November 10, 2020, 6:17 am

Does Sedera exclude rock climbing or other “high risk” activities?

Bill from The Fire Guild November 10, 2020, 1:43 pm

Hi Jill-

They do not exclude specific activities and in fact they (and we) love Members who exercise! This is their official language about what activities would not be eligible for sharing:

“Members understand that medical expenses resulting from the use of illegal drugs, or

while participating in unlawful activities, will not be shared.”

So, as long as you’re not trespassing while climbing, or under the influence of illegal drugs, climb on!

Victor February 24, 2021, 3:13 am

How are illegal drugs defined? For instances Cannabis is legal in my state. I use it most nights to get to sleep so I would definitely fail any drug test.

Bill from The Fire Guild February 28, 2021, 9:12 am

Illegal drugs are defined from the federal level. As mentioned previously, however, they’re not looking for ways to deny you. There is no “drug testing” and unless your drug use directly contributed to your reason for seeking medical assistance, they wouldn’t even know. AFAIK, no hospital drug tests their patients unless a crime is involved.

caryatis November 10, 2020, 8:36 am

If you’re considering this plan, please investigate further—the coverage is VERY limited, and MMM didn’t mention some big drawbacks. For example, you have to promise not to use illegal drugs, and expenses related to drug use are not covered. Expenses related to a child who gets in a car accident while high would not be covered. Treatment for mental health care is very limited. Abortion is not covered and I could not find info on birth control

>Members understand that medical expenses resulting from the use of illegal drugs, or while participating in unlawful activities, will not be shared…medical expenses incurred by a member child who is injured while he/she is under the influence of an illegal substance would not be eligible for sharing. Note: Does not apply to dependent children under the age of 16.

Also, if you get HIV or another STD, apparently you must “demonstrate” that the disease was not contracted illegally. I don’t understand how that would even work.

>HIV, AIDS, or other STDs contracted without breaking any applicable laws (e.g. blood transfusions or medical procedures) will be shared. Expenses for sexually transmitted diseases, including the HIV virus are otherwise not shareable. It is the member’s responsibility to demonstrate that the disease was not contracted illegally (e.g., sharing needles in illegal drug use).

(See link: https://sedera.com/wp-content/uploads/2020/04/Sedera-ACCESS-Guidelines-20200402.pdf)

Matt November 10, 2020, 12:07 pm

None of these sound bad to me. If you choose to use illegal drugs, any consequences shouldn’t be the responsibility of others. Abortion is something I think should be covered, but from an individual perspective it’s unlikely and not the biggest cost.

I haven’t actually used this or any sharing plan, so I don’t have any first-hand experience to share.

Bill from The Fire Guild November 10, 2020, 3:24 pm

Hi caryatis-

The Sedera health sharing community is just that: A community of people dedicated to staying healthy and helping one another when they’re not. The requirements and guidelines are very specific and clear – if you currently have insurance, ask yourself if your insurance guidelines are as transparent and up-front? I can tell you that in my experience they’re not; and anecdotal evidence about claims being denied by insurance companies are a dime a dozen.

I do appreciate that you took the time to look over the Guidelines in detail and that Sedera might not be aligned with your lifestyle.

With that said, I’ll try my best to answer your points one-by-one:

1. Actually, you’re partially right: If you’re breaking the law, then you’re not covered. As a Member, I *love* this feature – it’s called accountability and I like knowing that my fellow members are law-abiding citizens. If you’re sharing needles or robbing a bank, then I honestly don’t want to be responsible for your bad choices!

The part you’re incorrect on is about children: Dependent children under 16 are eligible for Sharing regardless of the activity or substances involved. This is specifically stated in the Guidelines that you linked to. Sedera expects children over 16 to be responsible to their parents and as such, should be making proper lifestyle choices to remain healthy. If you know your kid’s not going to make the right choices, then Sedera’s just telling you in advance that they won’t be shareable events. I think that’s fair.

2. Mental health is partially shareable, and just like with many insurance carriers, is limited.

3. Abortion is not shareable – again, just like with many standard health insurance plans. Abortion for the express purpose of terminating a pregnancy is considered by Sedera to be a non-essential surgery – it’s not a health issue per se. Not to belittle this highly-charged subject (or start an argument), but from a logical perspective it’s a similar procedure to any other non-essential surgery that does not cure an illness or medical condition and as such is not covered. Sedera is about sharing health, not sharing any and all medical expenses. Just like car insurance that doesn’t cover adding fancy wheels or cutting off the exhaust to make it sound different, Sedera doesn’t pay for voluntary surgeries.

4. Birth control is a prescription drug and there are lots of details about Rx in the Guidelines, but again, taking birth control voluntarily to prevent pregnancy, vs as a cure or treatment is not shareable. If prescribed as a curative medication, it IS shareable.

5. HIV/AIDS is shareable – as you pointed out. Proving how you contracted it might be a subject that you’ll need to address when/if you cross that bridge, but again, it’s fair for Sedera to clearly state that if you become ill while engaging in illegal activities, your needs are not shareable.

Again, it’s not right for everyone, but it’s a fantastic option and it’s working really well for me!

Jingjing Yu November 11, 2020, 9:35 pm

I like how Caryatis pointed out some of the stuff that I would totally take granted for (or assume they would have). It is definitely worth to read the pdf here. I like how your response is too Bill. I am not so sure about birth control being an ‘option’ and not covered but I agree, that this fundamentally is different from insurance, therefore should be approached differently.

Tim Wenger November 10, 2020, 5:29 pm

My. wife and I have used Sedera for the past 1.5 years and haven’t had any problems. We haven’t actually had to use the cost sharing, so I can’t speak to whether there is any nonsense in actually getting them to pay your bill, but in our limited experience the customer service has been solid, they are super responsive, and generally appear to be legit. Again, I haven’t been to a hospital since signing up.

BUT

There is always a slight thought that if I wreck myself snowboarding or get cancer, that I’m skeptical don’t have full faith in them to come through. No justified reason to doubt them, but even if they did pay the bill, the thought of receiving a massive bill with my name on it and having to trust them to take care of it when they have no legal obligation to, isn’t the most settling feeling.

Eric B November 10, 2020, 5:32 pm

Can you add a list of “cons” to this page as well (e.g. not legally required to pay) to balance things out a bit?

Jon from The Fire Guild November 11, 2020, 10:10 am

Hi Eric,

Pre-existing conditions (look-back period of 36 months) are not shared in the first year (15k in second year and 30K in third, fully in the fourth). If you live in Illinois, New York, Washington, or Vermont, then you can’t sign up. Subjectively speaking, some people will be bothered that some items are not shared, while others will be happy that they don’t have to pay for it in the form of a higher monthly price. Rx expenses might be one area that people have differing opinions about. In addition, signing up for Sedera does not shield you from state mandates (e.g. California). Since the federal mandate has been abolished, that no longer matters. You would have to do the math to determine if the cost savings from signing up for Sedera would overcompensate for any penalties. I’m sure there are as many cons as there are opinions that people may have about this model. It’s not for everyone.

I’ll ignore the fact that Sedera doesn’t have negotiated rates with providers because that means that that you’re not tied to a network, a positive to me. The dirty little secret in medical billing, as I’ve been told, is that most providers will accept a price negotiated in line with the Medicare itemized cost schedule. So there is a baseline to draw from even though sticker prices are all over the place. If someone knows differently, please enlighten us!

And bear in mind that there are a lot of gripes out there about traditional health insurance. The following article was a mind blower to me when I read it two years ago and it’s 100% worth your time: https://www.propublica.org/article/why-your-health-insurer-does-not-care-about-your-big-bills.

Getting back to the downside, I want to point out a key distinction between Sedera and insurance: Insurance is a contractual agreement between you and the insurer where the insurer assumes liability for your expenses. Legally, it’s an assignment of claims. Individual states regulate this industry heavily and require insurers to abide by certain mandated rules. So as with any contract, the government stands behind it and can force one of the parties into compliance. In that way, I think of government in this case as a form of collective insurance that makes sure that insurers will pay, and that gives us a collective reassurance.

Sedera, on the other hand, is a community of members voluntarily sharing each other’s large medical expenses. If you need a legally enforceable contract, then you’ll have to pay for traditional insurance. If you’re comfortable with the concept of mutual trust (guild and fraternal-based insurance pools in the 19th century were originally called mutual aid societies https://en.wikipedia.org/wiki/Mutual_aid_(organization_theory)#Mutual_aid_vs._charity but if you can accept a proven track record and trusted testimonials, then Sedera is something to consider. I haven’t heard of any eligible Needs being rejected or unpaid. And believe me, if there were bad news you would see it on the Better Business Bureau site (https://www.bbb.org/us/tx/austin/profile/health-care/sedera-inc-0825-1000131320). And speaking of complaints, I have something to say further below about my experience with Liberty.

The other drawback is that you’re a self-pay patient, as opposed to having all your billing handled by the insurer and doctor’s office (of course at a loss of efficiency). You directly pay your bills and Sedera shares the amount over the IUA for each individual need. They pay you back by check or direct deposit within 60 days. Becoming a self-pay patient turns you into a shopper for healthcare, and that’s something that Sedera highlights and something that’s flat-out foreign and kind of uncomfortable to all of us. It seems that when we all aggregate into huge groups, we lose sight of the fact that our expenses are costly to other people. So when I find a lower price for, let’s say, lab work, that saves you money too because your monthly contribution stays lower. I like the sharing model because it’s a vivid reminder that we are all interdependent. When medical providers raise prices because insurance companies can just raise premiums in order to pay for the higher price that medical providers charge because insurance companies can just keep…well all of us lose out.

On a personal note, I’m a former member of Liberty and so I know their story well. Having read all the complaints on the Better Business Bureau’s website and having followed media coverage, I’d say the problem with Liberty is generally not that they have rejected claims. My sense is that they’re just paying late and they’re overwhelmed. It’s important to remember that these health sharing organizations are not all alike. For instance Aliera/Trinity has been investigated because of misleading sales tactics and misinformation, but that’s the sole instance. Sedera, by contrast, tells you upfront that they are not insurance and makes you sign off on that fact in their enrollment process. As we keep saying, we don’t want people signing up who don’t understand this or for whom this is the wrong path. The mutual aid aspect is real to me. People signing up with the wrong idea or even in bad faith will ruin it for everyone else. Which brings me back to Liberty.

They’re the ministry that opened their doors up to a larger audience, loosening faith-based (Biblical) requirements, whereas the other grandfathered health share ministries didn’t. This is not to call into question their motives or sincerity. I never experienced anything untoward or sketchy from them. But it appears that the monthly amount they were taking in from members didn’t match the snowballing amount of medical costs being submitted to them. They just raised their rates a couple months ago, for example, to deal with that. I’m guessing that all the new members didn’t bother to act as self-pay patients and just handed their Liberty card (Sedera doesn’t provide one because we’re self-pay) to the front desks of doctors’ offices, which then billed Liberty full price. The real issue is that delayed reimbursements translated to members being sent to debt collection by medical providers. Super stressful. As Liberty delayed payment they got a bad rap among doctors and hospitals, which meant they were less likely to negotiate. But if you pay doctors quickly this problem largely disappears. Cash discounts exist because people love cash up front, and we don’t have to cite present discounted value theory to understand that. Sedera has a good reputation for timely payment.

The reason I left traditional insurance four years ago is because, not qualifying for any marketplace subsidy, my monthly premium for two 40-somethings and two kids was going to be $1,200. Add the $12,000 catastrophic deductible, and that meant that I was going to be on the hook for over $26,000 in the event of a large medical bill before the insurance company kicked in anything. Everyone has a tipping point. For some of my extended family members, that means not being eligible for Medicaid but deciding to go without insurance altogether even though medical debt would swamp them! Maybe you’re okay with a $1,000 premium at a $5,000 deductible. But what about $2,000 and a $14,000 deductible? That would be a $38,000 exposure. At some alternatives start to make more sense. It’s all about how much present value you are willing to forgo to hedge risk. Over the past 5 years, I’ve saved about $9,000 per year. I’ve been funneling that into the Vanguard S&P 500 fund, enjoying the rise of share prices and collecting (reinvesting) dividends. That snowballing post-tax money is available now if I need it, and Sedera gives me comfort that I have a reasonable good-faith hedge against ever actually needing it.

Sedera has been watching all of these developments unfold. They are growing membership organically, unlike other sharing organizations that do TV and radio ads, and unlike Liberty, which essentially took on all-comers. They have two entities: Sedera, Inc., facilitates member sharing, while the non-profit Medical Cost Sharing holds the money in trust. Money that goes into the non-profit can’t be taken out again by them or us. And they’re also not new to the health sharing game. Their bill negotiating wing has been operating for over two decades on behalf of other organizations and companies (self-insurers).

But what I find actually interesting, is that my own criticism of Sedera, as a business model, is that they’ve been too cautious in some ways. When Bill and I started investigating them two years ago, we spent hours on the phone with their sales reps. We both concluded that we love the model (I was already familiar with it through Liberty) but that they should be going whole hog direct to consumer to sign people like us up. At the time, they were only really doing employer groups and were bringing in individuals on a case-by-case basis, mostly through insurance agents. It’s only until this summer that they began actually enrolling individuals through their enrollment platform (via an affiliate like us). The reason why they’ve been so cautious is that they clear everything through their legal team and they check with regulators on how they do things. They wait for the regulators to say “we like that, no we don’t like that, you should use those terms, that doesn’t sit well with us,” and so on. They really don’t want to get on the bad side either of the public in terms of reputation, or with regulators. They’re not grandfathered under the ACA like the ministries (had to be in existence as of December 31, 1999). So they’ve carefully structured this sharing model.

So despite some drawbacks, combining DPC and Sedera (and Teladoc) is a nice way for me to cover my bases and I feel that the positives outweigh the negatives.

Eric B November 22, 2020, 11:23 am

Thanks (especially for the insight on Liberty).

I still feel like these health insurance alternatives are siphoning healthy people out of the traditional insurance marketplace, thus raising the costs for those who are “stuck” with traditional insurance (due to expensive conditions, need for asset protection, etc.). That feels like the opposite of voluntarily sharing large medical expenses.

Regardless, something definitely needs to give in the current situation, and maybe an out of control spiral where traditional insurance is only used by an increasingly sick/expensive group is the only way to force change…

Vince November 10, 2020, 6:30 pm

Are yearly well woman exams covered like pap smears and breast exams? No mention of those items on the membership guidelines PDF.

Jon from The Fire Guild November 11, 2020, 8:18 am

Hi Vince,

Sedera shares screening mammograms for ages 40 and above and screening colonoscopies for 50 and above (check out pages 30-31 of the Member Guidelines, available from the signup link at the top of this page). Yearly flu shots and childhood immunizations to age 18 are also included.

They don’t share in wellness exams in general though. That’s because Sedera is for when you have a larger medical expense (i.e., anything over your IUA – $500 to $5000, your choice). For lower cost expenses I visit my local direct primary care doctor and I’ve used Teladoc (that’s the telemedicine service that you can add on super cheap when signing up for Sedera: https://www.teladoc.com).

My own annual checkup is a full hour of just me and the doc discussing anything and everything. The reason I left a traditional large medical practice was because of the annual checkup. I liked my doctor, but the first thing he said when he came into the room was that he was sorry but this year he couldn’t talk about any issues aside from wellness. So any minor, non-urgent stuff I had saved up to talk to him about would have to be coded separately or a separate billable visit would have to be scheduled. And that really bothered me. And it bothered him if the long sigh right before he told me this is any indication. I’ve heard from lots of people who are equally frustrated by how the insurance companies and medical practice management teams are increasingly looking over doctors’ shoulders. Now I pay $60 a month and anytime I need to see my DPC doctor, I make a same-day appointment, bike over, and we address the problem. He’s never in a hurry and he’s not having to calculate what the insurers will think.

If you want a closer look at how it all works using DPC in combo with Sedera, click on this pdf download https://thefireguild.com/wp-content/uploads/2020/11/ACCESS.MembershipSummaryDPC.Telemed.V2.pdf

Aaron November 10, 2020, 6:48 pm

As an ER physician that used to have a house call business many years ago, I used to be really up on the insurance options. Insurance has always been a middleman scam to me. High deductible plans were the way to go back then, paying cash for all else.

This thing you’re talking about is fascinating to me. But, the one thing I’m wondering about is whether you run into having to educate every doctor that is not a DPC and “negotiate” a cash price before you are allowed to make appointments? In my experience, I’d call up, say, a dermatology office and the front staff (never having encountered anything but traditional insurance) would say that I couldn’t even make an appointment, or that they’d have to talk to the doctor first to figure out a cash price. It is just an extra hurdle and likely very worth it but it did get a little tiring always being met with a blank stare.

Have you had to navigate that, or have things changed in the era of concierge medicine? Either way, wonderful to see anyone successfully think outside of the cage regarding insurance and healthcare. Thanks.

Jon from The Fire Guild November 11, 2020, 3:36 pm

Hi Aaron,

It seems like you were ahead of your time on this. The cash pay approach is basically what you describe. Depending on where you live, you might get some blank stares. But I think more and more practices are becoming familiar with the model. There are over a million people enrolled in health share organizations in the US. And as medical costs have risen so much year-over-year, more and more people are having upfront conversations about what a medical procedure will cost. One nice thing about Sedera is that if you’re thinking about a procedure that goes above your IUA, you can call member services and have them call around for a price check in your area.

Here’s cool website to do some price checks on medical procedures: https://www.healthcarebluebook.com/explore-home/

By the way, I’ve heard the term concierge medicine used, but I think these days it’s for practices with higher-priced subscriptions. Direct Primary Care is more for regular folk at lower rates.

Sasha M November 10, 2020, 9:51 pm

1. Mental health is partially shareable, and just like with many insurance carriers, is limited.

It sounds like most mental health services will not be covered.

2. Birth control is a prescription drug and there are lots of details about Rx in the Guidelines. If prescribed by your health care provider as a necessary treatment for an illness, would be considered shareable.

3. HIV/AIDS is shareable – as you pointed out. Proving how you contracted it might be a subject that you’ll need to address when/if you cross that bridge, but again, it’s fair for Sedera to clearly state that if you become ill while engaging in illegal activities, your needs are not shareable.

Bill from The Fire Guild November 11, 2020, 2:21 pm

Sedera is not for everyone, and no one is suggesting it is.

They have 35K members and climbing, with zero complaints. Guess some people are ok with the guidelines.

I am!

:)

Terry November 11, 2020, 3:49 am

I have been looking at these options for 2 years now but sort of skeptical about the coverage. Coverage to me is medical, dental and vision and I’m not sure how this is handled via these shared insurance offerings. This may be a good opportunity for me to investigate this further as I can compare 2021 company insurance with the shared insurance.

Some questions I have:

– Has any one compared MediShare, Sedera and others?

– What are some good options for dental and vision? I was supposed to have an iridotomy procedure this year and my OOP expense was $3K !

– Can you fund an HSA account for these plans?

– Has anyone created a comparison spreadsheet?

Lastly; thank you MMM for education us on these money savings options that are usually hard to analyze individually.

Cheers!

Jon from The Fire Guild November 11, 2020, 3:50 pm

Hi Terry,

It’s a different mindset. It’s not insurance. The terms from the insurance industry and the terms that health shares use can be confusing. I recommend studying up and it will become clearer.

I think there are some sites out there that do comparisons, but I don’t know of one in particular that I can recommend.

Answers to your questions:

– Sedera doesn’t generally share in dental.

As for Vision (Optical), let me quote the guidelines:

“Shareable for expenses due to cataracts, glaucoma and other diseases or injury to eyes. Vision therapy subject to 25 visit maximum per Need, to a maximum of $2,500 per separate Need.”

As for Dental,

“Sedera members share: a. The breaking or injury of natural teeth and caps (but not repairs to dentures or partial plates) by accidents other than when eating and certain motor vehicle accidents. b. Operations on bones in the mouth (not teeth). c. Life-threatening dental problems.”

–Short answer on an HSA account is no. The longer answer is that Sedera has been lobbying the IRS to have their memberships recognized for HSA purposes. We’ll see where that goes. There’s also no tax deduction for your monthly contributions. When I was on traditional health insurance, I believe I was able to deduct one half of my premiums as a self-employed person. Not sure where that stands now.

– Not aware of any spreadsheet. We ourselves haven’t created one because their faith-based requirements rule them out, and because the less-strict Liberty has become unreliable.

LG in COS December 15, 2020, 8:25 am

Hey there, this is from an email reply on Dec. 3, 2020 my CPA gave me regarding tax deductions for the self-employed:

One other thing you may want to look into as an alternative to traditional health insurance via the marketplace is a healthcare sharing ministry. These used to not provide any tax benefits but recently were deemed eligible for the self-employed health insurance deduction. I have never participated in one because I have some pre-existing conditions and they do not have to cover them. It sounds like you may have found coverage at a decent price, but it’s still worth a peek to see if it would be a better fit. There are a number of them, but I am most familiar with clients going with Christian Healthcare Ministries, Medishare and I have one who has gone with Allera, I think it is or something like that. ”

So that is kinda cool.

Lisa November 11, 2020, 4:50 am

You had me – im not a big fan of insurance paperwork or stressed out docs. Then I got into the details..No coverage for maintenance meds beyond 120 days? No insulin, no cancer meds, no thyroid meds? My goodness. I guess that’s one way to carve the “unhealthy” out of your insurance pool. Drug costs and the last six months of life in a hospital, trying to “save” you, are the real financial bugaboos.

Bill from The Fire Guild November 11, 2020, 6:00 am

Hi Lisa-

If you read the guidelines, you can see that cancer meds are a shareable need separate from the 120 day rule. Also, they explain that the 4 months of Rx coverage is because Sedera is designed for healthy people who (and while I’m sure there are lots of arguments against this) generally only need meds to get past a health event (think: antibiotics, anti inflammatories, etc). If you’re on a medication for longer than a quarter of a year, it seems like this would fall under the category of a chronic situation and you’re absolutely right: Sedera generally does not share chronic health issues.

Just like someone else succinctly analogized car insurance to not covering oil leaks or slipping transmissions, Sedera also does not share ongoing body maintenance (generally).

They are very transparent about this, with clear, layperson’s-terms writing so you know what you’re getting when you sign up.

As for the last six months of life in a hospital, aside from the Rx costs, can be a shareable event – nowhere do the guidelines stipulate that it isn’t.

Also, since I’m writing this as a real live person, and I don’t work for Sedera (or anyone; I’m retired!): It’s in fact a terrible part of our total US health care system that 90% of our healthcare dollars are spent on the last 1% of our lives. We need to move away from the undignified, drug-filled, frantic end-of-life and toward a peaceful acceptance of the only universal truth – death.

Laura November 11, 2020, 5:34 am

Doesn’t sound like it would work for me. Currently paying $400/mo for insurance. Three years ago I had a hip replacement. Cost? $107,000 and that was only the hospital’s part. Insurance paid the total cost. Would Sedera. I do strongly support concierge medicine.

Bill from The Fire Guild November 11, 2020, 6:06 am

Hi Laura – congrats on the new hip!

I don’t work for Sedera, but I know their guidelines pretty well and I can loosely say that yes, a non-elective hip replacement is a Shareable event with Sedera. You’d be responsible for your IUA (which you choose and can be from $500 to $5000) and the balance would be shared.

I am 52, my wife is 53 and they accept members up to 64 years old.

Dan P. November 11, 2020, 6:31 am

Bill – Thanks for taking the time to address questions. My primary concern regarding Sedera, based on my detailed experience with Liberty healthshare, is how operationally efficient they are. The challenge with the healthshare model (regardless of religious affiliation or not) is that they mostly do not have formal relationships with medical providers. Sure, some may, but most medical providers (for example, the ones we use in Cleveland) do not have formal relationships. Thus, the medical provider sends you a bill directly and when we submitted it to our healthshare they’d request a bill with additional detail (i.e. the specific medical codes). So we would need to call our medical provider, ask for the detail, wait 2 weeks and re-submit the bill which re-starts the clock. Every medical provider will bill in a different format with different levels of detail. The medical provider is not going to remember every time they send you a bill that you need it in a special format. How does Sedera deal with this practical challenge? The point is, regardless of how efficienct Sedera is once the correct bill format is submitted, healthshare members need to detail with the inefficiency of medical providers, which effects their overall experience. Liberty had their unique issues providing transparency into the status of reimbursement – it took them very long to process the bill even once it was submitted correctly. Again, some of this is certainly unique to Liberty but I do think there are practical operational challenges any healthshare might run into. Any thoughts from you or other Sedera members on these challenges?

MP November 11, 2020, 11:49 am

My experience with Liberty Healthshare was good, but they took an age to process claims.

Jon from The Fire Guild November 11, 2020, 5:04 pm

Hi Dan,

I remember you and your blog. I just posted at length above, including about Liberty, in response to Eric B and touched on some of these issues. Liberty definitely had issues with the onslaught of new members. I recall talking to someone there at one point and it was clear that they didn’t have a handle on bills being submitted. Members would submit bills with insufficient coding and they would have to go back and forth. Just as you described. Their new portal had fields that require you to enter certain information. I haven’t heard of similar issues with Sedera. You basically scan or take a snapshot of your bill and upload it to their portal. The people there have been involved in medical negotiation for a long time—predating their incarnation as a sharing organization—so it’s a strength of theirs.

Dan P. November 12, 2020, 1:43 pm

Jon – Thanks for the response. Pretty fair assessment of Liberty. I also felt they were completely overwhelmed and did not have the operational processes to manage billings. They have grown too quickly. I may call Sedera to talk to them about how they handle the lack of detail/codes that exist in a normal medical bill. There’s a brief description, but not a specific code, so I’m wondering if they require a specific level of detail. I agree, once you get the right bill it’s a simple process to upload the bill but if your medical provider doesn’t provide the right format that could be a problem. I’ll follow-up directly with them. Thanks.

Jon from The Fire Guild November 12, 2020, 2:36 pm

Dan – The phrase they use for submission requirements is “original, itemized bill.” The Member Welcome Packet says “Itemized statements list the exact services and prices that you received. Sedera will not accept any documentation that does not include specifics. The following is an example of an itemized statement.” And then what follows is a screenshot of a basic itemized bill (without a CPT code). I know they do like to have the CPT code when you call member services in advance of a non-emergency procedure to have them research pricing in your area.

Joanna November 11, 2020, 4:07 pm

Does Sedera negotiate cash prices on member’s behalf for the self-share portion? Or are members required to pay the astronomical cash rates?

In my experience, cash prices are always significantly higher. I initially tell them I don’t have insurance, wait for the bill, then add the insurance. So I know what the cash prices vs.pre-negotiated rates are.

The only exception so far are Walmart’s $4 prescriptions (same price with, or without insurance), which is cheaper than the pre-negotiated rates at any of the traditional pharmacies.

Jon from The Fire Guild November 11, 2020, 5:26 pm

Hi Joanna,

Sedera would take action above and beyond your IUA. For a non-emergency procedure, you’d call them in advance and coordinate with them. If you’re paying cash, you would never pay more than your IUA upfront—to let them negotiate the rest. For something under your IUA, you’d shop around. Sounds like you have experience with cash-pay. Joining a DPC is great for a lot of basic medical issues. You could always keep your IUA level at a low $500, but your monthly contribution of course would be more. This site might be a good resource for you.

https://www.healthcarebluebook.com/explore-home/

As for prescriptions, Sedera’s putting the finishing touches on an online Rx marketplace with some cool features/options:

1) Using a retail discount card (like GoodRx) to check pricing in your area with over 67,000 pharmacies in the network, 2) Home delivery, 3) International pharmacy (i.e. delivery from Canada and other countries), 4) Prescription assistance program for those who qualify.

Chris November 12, 2020, 8:50 pm

One of the first posts asked about “risky activities” and if they’re covered (the example was rock climbing). I’m glad to see that it is.

However, I think my personal concern would be how much “legality” is used to skirt having to make share payments.

I understand we don’t want to support illegal activities, and I think that generally makes sense.

That said, the dumb crap we humans sometimes do is the most risky—and often technically illegal, even if something like a misdemeanor minor offense.

I’d love some clarity on this.

I’ll throw some random examples out:

– Assault/battery are illegal acts—if I get into a too rough of a fisty-cuffs with a buddy, will a broken bone not be covered because technically we engaged in an illegal activity?

– Trespassing is illegal, but all too often the sort of risky physical activities that are dumb (and risky!) occur while trespassing even if it’s generally unintentional (mostly just not knowing where you are), think: 4 wheeling, rock climbing, water sports, exploring an abandoned warehouse, etc.—if I slip while hiking a shortcut across some guy’s farmland and break an ankle, I’ve committed an illegal act through trespassing—am I SOL on the share?

– Adultery is illegal in countless states, if the adultery were to pick up an STD during such an act, would related medical procedures not be covered?

– If I’m driving on a suspended license and have a heart attack in the middle of traffic, will the heart attack not be covered? Let’s assume I’m ticketed for that offense before being carted off by ambulance.

– Illegal drugs have been batted around a lot and are a great example. I wonder if merely being under the effect of an illegal drug and then having some medical issues occur (entirely unrelated to the drug) would cause any share to be invalidated for that medical issue.

I’m sure I could come up with a ton more examples.

I looked up how health insurance applies to the same question and found this great explanation:

“The basic rule of insurance is carriers will not cover an insured for intentional illegal acts. Insurers will cover patients for harm resulting from their illegal act IF that crime was not intended. Therefore, if a driver is injured while trying to run down his neighbor that driver will not be covered. But if the driver drove while drunk – itself an illegal act but without intention to commit a crime – he would be covered for injuries he sustained when he crashes into a lamppost.”

I’m wondering where health shares fall on that spectrum. From my reading of it, I fear it might be more conservative (so as to not cover the lampost crash injuries in the example).

I’d love to see if we could get an answer about this sort of a thing via the Fire Guild. Cheers!

Jon from The Fire Guild November 13, 2020, 8:14 am

Hi Chris,

This is like an ethics class. Cool! Sedera goes off the police report/accident report. So there would need to be an official record of whatever that unlawful activity is.

If you get into a fight with your buddy, there wouldn’t be such a report. If you’re trespassing, I assume you’d limp your way off that property and drive your butt to an urgent care clinic. Where’s the report?

Would your doctor ask about the origins of your STD? From Sedera’s Guidelines: “HIV, AIDS, or other STDs contracted without breaking any applicable laws (e.g. blood transfusions or medical procedures) will be shared.”

If you’re driving on a suspended license, and there’s an accident then there would be an accident report. Maybe even a police report. You’ve clearly broken the law when the law told you not to drive. Like drunk driving. So I’m guessing you’d be on the hook. If you are on a suspended license, had a heart attack, and crashed into a telephone pole without harm to anyone else, then that seems like a gray area and, again, there would need to be some report.

Sedera refers to federal law when considering if a drug is illegal. That’s obviously an important distinction because many states are legalizing certain previously illegal drugs. (This is an interesting consequence of our constitutional structure as a federation of states with their own lawmaking powers). Let’s say you were high and you suffered an unrelated medical issue. There would have to be some kind of documentation from an authority or a medical provider. Will the doctor test you for drugs? Would privacy laws allow a medical provider to divulge the presence of illegal substances in your body? I once served on a jury adjudicating a knife fight and as jury members we were not told that the perpetrator was high on PCP!

The intent of Sedera’s rules are clearly to wall off certain behaviors that are more likely to cause injury and illness than other behaviors. And as you discovered from that health insurance quote, intent is huge in the law. As a member, you join the community with the intent to keep everyone else’s costs down. By forgoing certain behaviors–illegal ones–you are more likely to do that. The other goal is to have members appreciate their interdependence in a more tangible way. To me, this thinking seems almost entirely lost in the insurance industry. None of the parties seem to be thinking about the consequences of their actions on others. Ultimately, it comes down to your freedom to act but your moral duty to accept the attendant consequences.

I have no evidence or reason to believe that Sedera would nickel and dime you on the fine print. It’s not their money. For-profit insurance companies get to keep (and spend) every dollar they claw back from claimants in the form of denied claims. Sedera Inc. takes its fixed cut, and the rest of our monthly contributions are held in trust by a nonprofit. The corporate entity just moves the money around on our behalf. So if your need is rejected because you violated the rules, then that actually protects the other members.

A lot of this comes down to the letter versus the spirit of the rule. In part, it’s a matter of conscience. The question to ask oneself is am I trying to get away with whatever I can or am I trying to help the community out?

Chris@TTL November 13, 2020, 9:00 am

Jon,

Appreciate the follow-up! It’s helpful in understanding how the system works.

I think I got the answer I was looking for, though I suppose I was looking for a more distinct answer.

It seems fairly clear that with health insurance that intentionality is what affects coverage in terms of legality. I still don’t know if that’s the case with health shares (or even Sedera) with your response.

I *think* you’re suggesting that my initial reading was correct, any illegal activity (whether directly related to the healthcare event itself) would disqualify someone for a share—technically. Whether that’s actually happened that you know of or not.

I understand what you’re saying about my random examples, eg: you’d hopefully walk (limp) off someone else’s property if you were trespassing before calling an ambulance. Or that your doctor likely wouldn’t ask (or you could lie) about the origins of an STD (so far as how the illegal act of adultery might affect coverage).

However, it wasn’t my suggestion that you’d ever try to “cover-up” these illegal acts in order to maintain coverage. I was merely inquiring what is actually the policy in these cases—not how to avoid not being covered/shared. I wasn’t asking an ethical question.

To your point:

“The question to ask oneself is am I trying to get away with whatever I can or am I trying to help the community out?”

I’m not sure if you’re asking that as a pointed question for me or for the general readership, but I’d suggest people shouldn’t be trying to skirt policy or the law.

I merely wanted to know the answer—perhaps I’ll find it by digging into policy documents for Sedera more thoroughly. Thanks for the follow-up.

Jon from The Fire Guild November 13, 2020, 12:04 pm

Hi Chris,

No, this point was being made in a more general light without targeting you. I wouldn’t want to be challenged to a virtual duel by impugning your character!

From the Sedera guidelines: “Among other things, Members understand that medical expenses resulting from the use of illegal drugs, or while participating in unlawful activities, will not be shared.” Intent appears to be irrelevant. Participation is the factor. Drunk driving, for instance, disqualifies you.

Joanna November 13, 2020, 12:21 am

How does this work for pregnancies? Is there a waiting period? Does the mother have to be on the plan? Or is it enough for one parent to be on the plan? Are there any limits for the newborn and are the costs sahred starting from birth?

Bill from The Fire Guild November 13, 2020, 12:39 pm

Pregnancies are shareable, with some restrictions.

The biggest is for pregnancies that occur within the first 90 days of membership; they are not shareable.

Also, regardless of your IUA, maternity costs have a separate IUA of $5K (you’re responsible for the first $5K of expenses, the balance is shared).

Many healthshares have had difficulties with people unscrupulously joining just for their maternity costs, then leaving immediately after. This is not how a community is sustained, so Sedera has come up with a semi-solution with these restrictions. It’s imperfect, but helps the community to keep costs lower.

Sedera memberships choices are: Member only, Member + Partner, Member + Children or Member + Family.

The mother has to be on the plan for coverage of maternity costs.

There are no limits with Sedera, for maternity coverage or otherwise (Unless it’s for a pre-existing condition as explained in other comments).

I hope that answers your questions.

Jon from The Fire Guild November 13, 2020, 3:15 pm

As for newborns, the Sedera Guidelines state in section 9 (“Maternity Needs”):

“9.4. Newborns will be included within the household membership retroactive to the date of birth as long as the Member notifies Sedera, Inc. to add the child to the membership no later than 30 days after birth.”

And then this:

“9.A.2. Bills for all pregnancy and birth-related complications of the mother will be shared as a part of the maternity Need. Routine postnatal care of the child, including no more than one routine outpatient doctor visit, will be part of the mother’s maternity Need. Any pre-birth Need of the child or a post-birth Need of the child beyond routine natal care will be considered a Need separate from the mother’s maternity need.”

So the child would be subject to a separate IUA as a distinct family member apart from any “routine natal care.”

Here are the guidelines: https://assets.ctfassets.net/01zqqfy0bb2m/7LTd6ptiu0KMF7xoQBpX5a/10ce32f0ecc5da6ba271d37a3743a876/Sedera_-_ACCESS_Plus_Guidelines_20210901.pdf

Eddie November 13, 2020, 7:01 pm

Hi Bill,

This is a fascinating concept and overall I love it. Since this is all about members sharing expenses (a co-op vs. an apartment, if you will), is there a mechanism by which members can vote to alter the rules? Re: birth control and abortions, for example, if enough people think they should be covered full stop how could that change be made?

Thanks for all the info!

Bill from The Fire Guild November 14, 2020, 10:08 am

Hi Eddie-

This is an interesting question and begs the further ponderance: What keeps a group of like-minded individuals from forming their own “benevolent society” for sharing healthcare expenses?

The answer is: Nothing! If enough Mustachians (for example) wanted to form their own collective, there’s nothing stopping us! And in fact that’s how Sedera started – a group wanted a non-religious option for sharing medical costs. (and we could make all sorts of cool rules like we pay all costs associated with bike accidents AND give you the money for a new bike!)

To answer your question specifically, there is a board within Sedera that works on subjects like this. Sedera has been in business for 6 years, and the founder has been involved with health cost negotiations since the 90s. I suspect (this is just a guess on my part) that this subject has been addressed before (and will again) and so far, they’ve found that their current approach works best for their customers. They clearly explain, in straightforward language, their policies and as you’ve already read, Sedera is not for everyone.

With that said, I can tell you that I agree with Pete completely about the intelligence of making birth control available to all (worldwide and for free!) and that Planned Parenthood is a great way to support that idea.

Mike V November 14, 2020, 5:20 am

I supposed hypertension or high cholesterol would be considered pre-existing condition right? In that case, how would ongoing Rx costs be handled? And what if one has a heart attack or stroke within the first year of Sedera, would the costs be not-shareable because of the pre-existing conditions above?

Jon from The Fire Guild November 16, 2020, 11:31 am

Mike V,

Any condition with a diagnosis or symptoms (even symptoms indicating a suspected condition) would be considered a pre-existing condition. So hypertension and high cholesterol fit that category in terms of treating those specific conditions. You’re not excluded from joining Sedera with a PEC, but the PEC is only shareable with limitations (1st year no sharing, 2nd year sharing limited to 15k, 3rd year 30k, 4th year fully shareable).

There are two categories of Rx costs with Sedera: maintenance and curative. Maintenance would be for things like chronic conditions where the medication is used to maintain your health. Sedera only shares in such conditions if they are newly diagnosed after you join and then are limited to 120 days. Curatives are meant to cure a specific condition, and you would stop taking the drugs as soon as the condition was cured. So as long as you met your IUA for that overall need, the curative drugs would be rolled in to any sharing amounts you received for that. In other words, for a knee surgery, pain meds would be included along with crutches, the surgery, etc. But Sedera offers Rx resources for people who need prescriptions drugs (retail discounts, home delivery, international pharmacy and an assistance program for those who qualify). That member resource is here: https://therxmarketplace.com.

Most hypertension or high cholesterol conditions are being treated by maintenance medication and that would be considered treatment. Therefore, this pre-existing condition would be subject to sharing restrictions. If there is a big event in the first year of membership, there would be no sharing for that specific condition. If there is no PEC or treatment (aka medications/doctor visits) or symptoms, then it would be shareable beyond the IUA.

Here’s some language from the Guidelines (https://thefireguild.com/wp-content/uploads/2020/11/Sedera_-_ACCESS_Plus_Guidelines_20200901__MCS403.pdf):

“7.A.2. Verification for certain conditions: For some conditions listed below (all of Section 8 and Appendix), a written verification signed by both the Member and the Member’s treating physician must be submitted to substantiate that there have been no signs or symptoms of the condition, no treatment needed, no medication recommended or taken, and no suspicion by the patient or doctors that the condition was resurfacing for at least 36 months prior to membership effective date.”

“8. Heart conditions: Shareable. During the first three years of membership the statement described in Section 7.A.2. must be provided. See high blood pressure exception below. Sharing limits stated in Section 8.A and 8.B. will apply if a need request is determined to be a medical condition that existed prior to membership.”

“10. High blood pressure: Shareable. Provided the member has not been hospitalized for high blood pressure within three years prior to membership and has been able to control this condition through medication and/or diet. An incident that begins after membership becomes effective is shareable and would qualify for one 120-day period for sharing of prescription expenses (See Section 8.B.35.) Medication thereafter for maintaining a chronic condition is not shareable.”

And here’s an overview of Sedera membership:

https://thefireguild.com/wp-content/uploads/2020/11/ACCESS-MCS-Overview-10_2020-2.pdf

Kay November 15, 2020, 2:43 pm

Can this work with a HSA? Or would it make sense to use a High Deductible insurance plan with a DPC and HSA?

Jon from The Fire Guild November 16, 2020, 10:01 am

Hi Kay,

I’m reposting my (modified) message from the comments section of the MMM article on this same topic:

You can’t currently use money from an HSA (Health Savings Account) to pay for a DPC (Direct Primary Care practice). The IRS regards DPCs as a form of insurance (I suppose because you’re paying for a possible, future medical event). Nor can you set up an HSA based on your being a member in a health share (like Sedera). The American Academy of Family Physicians (AAFP) writes the following on its website: “”Under existing interpretation of the Internal Revenue Code, patients with HSAs are prohibited from engaging in DPC arrangements with a family physician or other primary-care physician.” (https://www.aafp.org/news/government-medicine/20190826pceact.html)

So you can only have an HSA with a high deductible insurance plan. The model suggested here is to sign up for a local DPC and to enroll in Sedera. Sedera’s CEO has been trying to get the IRS to change their stance and allow HSAs for Sedera members.

Greg November 23, 2020, 8:06 am

Looking at DPC and Sedera also for myself and my wife. I am retired and have a HSA that will pay for MY bills and prescriptions, my wife’s expenses aren’t covered because we were not married at the time of my employment. A person on the DPC/Sedera (Healthshare option) is paying for healthcare needs out of pocket that were negotiated at a cash rate with the provider and should get reimbursed from HSA for these expenses? With the exception of DPC/Healthshare subscriptions. Not ideal but a possible workaround?

Jon from The Fire Guild November 23, 2020, 2:35 pm

Hi Greg,

That’s a really good point. You can pay for any eligible medical costs with your HSA money and then submit that need to Sedera for sharing. And a quick Google search tells me that if you’re ever able to claim your wife as a dependent, you could cover her costs out of the HSA too.

Sean January 27, 2021, 2:00 pm

The Trump administration ruled in 2019 that you can no longer use existing HSA funds to pay for DCP fees. According to this website “The rule explains that in this circumstance, DPC generally provides access to services before the application of the HDHP deductible that goes beyond the scope of what the IRS considers to be preventive care and meets the standard of other health insurance” https://www.mzqconsulting.com/blog/new-irs-rule-has-pros-and-cons-for-direct-primary-care

Stephen November 17, 2020, 6:56 pm

We are a family of four in California, self-employed and we do not qualify for ACA subsidies. This year our insurance premium for the highest deductible ACA Bronze plan went up to $1,333 per month. The insurance article by MMM came at the perfect time so thank you for this! The discussion here is fantastic! I am a family practice provider so I have the advantage of being able to provide a certain level of care for my own family. I have also seen far too many people go bankrupt from not having insurance, so this is not an option. This combo of a DCP and Sedera seems like a perfect solution. While doing my research it appears that our family of four would owe $7,276 in ACA State penalties for not having traditional health insurance. This pretty much eliminates any cost savings we have with Sedera. I am wondering if anybody else is looking at this when comparing these plans? Am I missing something. Does Sedera exempt us from the ACA STATE health insurance penalty?

Jon from The Fire Guild November 18, 2020, 8:37 pm

Hi Stephen,

Membership in Sedera does not exempt you from any individual mandates at the state level. These mandates currently apply in Massachusetts, New Jersey, Vermont (where Sedera is not available), California, Rhode Island, and the District of Columbia.

Roberta Butterfield November 20, 2020, 1:19 pm

Is there anywhere to find the mentioned Medicare itemized cost schedule?

Absolute pet peeve after a broken clavicle and 2.5 years of cancer treatments for my spouse that no one can answer “How much will this cost?”

Bill from The Fire Guild November 22, 2020, 9:15 am

Unfortunately (and for reasons you can probably imagine), it’s very difficult to find the Medicare price list. If you search the web, you can find parts of it, but they’re often out of date. I have tried, over my years of “health insurance hacking” (including some medical tourism outside the US) to find a definitive list but it’s elusive. The other problem is that if/when you find a list, it’s very hard to nail down the exact procedure without the CPT code (and even then, sometimes the hospital or provider will have a code of their own that includes several other codes within it, in order to

obfuscateincrease efficiency.The lack of a definitive answer to your simple question: “How much will this cost?” is the single biggest issue in health care in the US.

For these reasons, I switched to a DPC (where they just do all they can to help “fix” me, at a flat fee – no bills to interpret, no arguments, and super-low admin costs for them!) and to Sedera who unlike a insurance company, is on MY SIDE to help get to the bottom of pricing and negotiate on my behalf, without any back-room arrangements or in/out-of-network BS contracts. It’s as transparent as one can get these days!

Blake November 20, 2020, 4:24 pm

Is there any concern about this essentially still being a startup healthshare company of only 4 years? I love the fact that there is the non-beliefs section of Sedera as I have to fudge things a bit with Christian Healthshare Ministries, but at least CHM has been around since 1981 and has rave reviews from Dave Ramsey and other in my circle. I guess for me, I don’t generally invest with someone who hasn’t been through at least a recession or two, and I tend to feel the same way with my healthcare. Any way you are able to come to terms with this?

Jon from The Fire Guild November 22, 2020, 10:02 am

Hi Blake,

I understand. You’re probably a reader of this blog precisely because you’re a rational sceptic.

Sedera was founded in 2014 (6 years in operation) but evolved out of a medical bill negotiating company that has been around for over 2 decades working for companies, organizations and self-insuring groups (and one that negotiates bills for Sedera members). In fact, they’ve also been negotiating the bills of one of the major health share ministries for over 16 years. So they know what they’re doing.

Personally, I’ve never heard of any complaints and haven’t seen anything on BBB over the years. They’ve always paid for eligible needs and have never had to tap the funds set aside for super-high (and rare) medical cases. They were also nominated for BBB’s “Torch Award for Marketplace Ethics” this year. They share funds with members usually within 30 days, sometimes within 60 if they have to negotiate. Customer service picks up the phone in Austin every time I call. And I have friends with Liberty who are in collections for past-due bills, for example, and can’t get through to them. With Liberty, bad news traveled fast and it didn’t take a full economic cycle for that to happen. The marketplace hasn’t sent up any red flags about Sedera over all that time.

The higher-level issue for me is that this model (insuring risk) isn’t all that complicated. They’re not building self-driving cars or rocket ships to Mars. They’re forming a risk pool and collecting monthly contributions. The actuarial math might be complex and beyond my abilities, but after that is figured out, all you need to do is move the money around. And I think the reason why almost every religious health share is doing okay is because it’s not that (comparatively) hard to run this model. You set monthly inflows to cover your outflows based on statistically predictable events. Insurance companies can always (and do) raise rates. These massive for-profit companies have no incentive to keep medical bills down and no incentive to keep your premiums low. And there’s little competition going on to keep them in check. And, honestly, what we’re seeing is that the health shares, although they’re not legally insurance, are offering an alternative model, i.e. competition.